Introduction

The Sustainable Sportswear Market covers apparel, footwear, and sports accessories made using environmentally responsible materials, low-impact manufacturing systems, ethical labor frameworks, circular design, carbon-controlled logistics, water-efficient dyeing, recycled polymers, bio-based synthetics, plant-derived fibers, toxin-free finishing, and production governance aligned with sustainability standards.

Sustainable sportswear includes organic, recycled, and regenerated material classes such as recycled polyester from post-consumer bottles, recycled nylon from fishing nets, organic cotton, hemp, bamboo viscose, eucalyptus-based lyocell, recycled elastane blends, natural rubber soles, algae-infused foams, bio-TPU coatings, and fabric ecosystems engineered for durability, moisture regulation, athletic performance, and environmental compliance.

This market has global importance because the sportswear industry serves a large user base: professional athletes, fitness consumers, sports clubs, outdoor enthusiasts, wellness communities, schools, institutions, and retail buyers increasingly selecting responsible product lines. Sportswear has shifted from a performance-only purchasing model to a combined performance-and-sustainability purchase framework.

Sustainable sportswear supports national decarbonization strategies, corporate ESG compliance systems, microplastic reduction roadmaps, chemical discharge safety rules, waste-reduction policies, responsible material traceability engines, and global pollution-control commitments.

The market is relevant because sustainability now influences product eligibility scoring in sports sponsorships, institutional contracts, retailer procurement systems, lifecycle compliance metrics, investor capital allocation, consumer loyalty indices, and long-term brand equity intelligence.

Learn how the Sustainable Sportswear Market is evolving—insights, trends, and opportunities await. Download report: https://www.databridgemarketresearch.com/reports/global-sustainable-sportswear-market

The Evolution

Historical Development

The early sustainability movement in sportswear began in the 1970s–1980s when natural fibers were used mainly for comfort, not environmental intent. During the 1990s, synthetic sportswear scaled rapidly due to rising performance demand, mass retail expansion, global sponsorship deals, and accelerated fast-fashion supply models.

Between 2005–2015, the first mainstream “eco sportswear” lines emerged, supported by organic cotton supplier scaling, polymer recycling R&D, early microplastic policy agitation, sustainability forums, and environmental advocacy pressure targeting large apparel brands.

After 2016, sustainable sportswear moved into commercial scale growth enabled by:

-

Recycled polyester scaling

-

Regenerated nylon from ocean waste

-

Waterless dyeing technology pilots

-

Blockchain traceability for recycled polymer chains

-

Carbon footprint scoring dashboards

-

Consumer compliance labeling systems

-

Circular and resale model pilots

Key Innovations and Milestones

-

Recycled Polyester Expansion (2010–2014): Major brands commercialized r-PET fibers.

-

Regenerated Nylon Adoption (2013–2017): Fishing-net and ocean waste reuse.

-

Bluesign and ZDHC Compliance Pressure (2015+): Restricted hazardous chemicals in manufacturing.

-

Waterless and Low-Water Dyeing (2016+): CO₂ dyeing pilots, digital printing, foam-dyed yarns.

-

Carbon Labeling Pilots (2018–2022): Product-level emissions scoring.

-

Athleisure Sustainability Push (2019–2024): Everyday wearable sports garments optimized for circular design.

-

Bio-Based Performance Elastomers (2020+): Castor oil-based polyamides, sugarcane-based EVA midsoles, bio-TPU films.

-

AI-Based Pattern Optimization (2021+): Yield improvements and waste elimination in cutting rooms.

-

Take-Back and Resale Infrastructure (2022+): National retail pilots for reverse logistics.

-

Algae-Infused Foams & Bio-Rubber (2023+): Used in footwear and composites.

-

Microfiber Capture Filtration (2023+ in select plants): Laundry and disintegration control at production scale.

Demand and Technology Shifts

-

Demand Shift: performance sportswear → performance + sustainable index scoring.

-

Material Shift: petroleum-dependent polyester and nylon → recycled and bio-based polymer systems.

-

Technology Shift: conventional wet dyeing → low-water systems → waterless CO₂ pilots, foam dyeing, digital printing.

-

Governance Shift: brand marketing sustainability claims → audited supply data → carbon-labeled products.

-

Retail Shift: first-hand sales → resale + take-back + lifecycle utilization frameworks.

-

Performance Engineering Shift: seasonal trends dependency → durability + lifecycle-extension manufacturing contracts.

Market Trends

1. Consumer Preference for Verified Sustainability

Consumers and institutional buyers increasingly score product lines using criteria such as recycled material share, microplastic shedding rate, carbon footprint per unit, dyeing system impact, chemical compliance credentials, durability index scoring, ethical governance, circular model eligibility, and transparency audits.

2. Growth in Recycled Polymer Blending

r-PET polyester and regenerated nylon dominate most scalable material pipelines. Recycled elastane remains limited but key investments are emerging for improved recovery.

3. Waterless and Low-Water Manufacturing

Waterless dyeing remains pilot-controlled due to capex costs but its adoption intent is growing in Europe, North America, and parts of APAC. Foam-dyed yarns and digital printing scale faster due to lower barriers compared to CO₂ systems.

4. Bio-Engineered Performance Fabrics

Bio-based polymer integration, plant-derived lyocell solutions for sports jerseys and activewear, natural rubber and sugarcane EVA blends for footwear, algae-infused composites, castor-oil polyamides, corn-based and CO₂-enabled midsole foams show increasing R&D adoption.

5. Microfiber and Microplastic Mitigation

Microfiber capture filters built into supply assessments, new yarn-treatment and finishing systems, tighter filament strength modeling, anti-shear knit architecture, nano-web bonding that reduces disintegration, athletic fabric structures scoring for microplastic risk mitigation influence B2B procurement scoring.

6. Transparency Infrastructure

Serialized batch authentication using QR, green labels, chain of custody tracing, carbon-per-SKU scoring dashboards, factory viability scoring, emission modeling systems integrated into procurement negotiation, AI-identified demand cycles based on region and sport class increasingly influence investment tiers.

7. Segment Expansion in Team and Sponsorship Clothing

National teams, sports franchises, outdoor sport clubs, marathons, fitness competitions increasingly sign managed sustainable sportswear contracts, including uniforms made using minimum recycled polymer eligibility scoring and carbon-labeled jersey product lines.

8. Regional Demand Patterns

-

North America: recycled polyester dominance, natural rubber footwear share expansion, ESG-led procurement.

-

Europe: policy-driven carbon compliance, retailer mandates, slow but high-value innovation contracts.

-

China & India: high volume athleisure sustainability lanes, rapid adoption of foam-dyed yarns.

-

Japan & South Korea: focus on supply-chain governance scoring.

-

Latin America: natural rubber + sugarcane EVA interest for footwear, agricultural fiber adoption pilots.

-

Middle East: focus on retail import viability for green sportswear.

-

Africa: growth intent accelerated by population demand but cost-limited by raw material corridor imbalance.

Technology Adoption

-

AI yield optimization

-

Waterless dyeing pilots

-

Foam-dyed yarns

-

Digital printing

-

Recycled polymer blending and knit finishing

-

Bio-rubber composite footwear production

-

Distributed modular plants for small batch sportswear suppliers

-

Carbon scoring and product labeling infrastructure

-

Ocean waste-enabled nylon supply adoption

Challenges

1. Regulatory and Compliance Complexity

-

Sustainability claims increasingly require audit verification.

-

Countries vary in accepted certification systems.

-

Retailer mandates for eco labels differ globally.

-

Microplastic regulations for synthetic textiles influence material eligibility.

-

Chemical discharge rules tighten formulation and finishing systems.

-

CO₂ dyeing adoption is slowed by multi-layer compliance approvals.

2. Economic Pressure

-

Bio-based polymers cost 1.8x–3x more than conventional petroleum synthetics.

-

Recycled elastane recovery is limited and expensive.

-

CO₂ waterless dyeing has high capex requirements.

-

Small sportswear suppliers struggle to compete with consolidated brands.

-

Raw-material price volatility influences margin safety for green sportswear segments.

-

Consumer willingness to pay premiums varies by region.

3. Supply-Chain Barriers

-

Limited recycled elastane.

-

Biomass polymer scale corridors remain uneven.

-

Logistics networks need carbon-controlled packaging, reverse-chain flows and circular infrastructure.

-

Take-back systems increase complexity for apparel logistics.

-

Warehouse safety and flammability compliance increases for bio-foam and natural rubber storage.

-

Modular plant deployment still requires environmental approvals and supply-chain integrity mapping.

-

ESG traceability requires data infrastructure compatibility among suppliers.

-

Ocean-waste recycling corridors are limited in select countries.

4. Market Risks

-

Certification fraud risks create buyer hesitation.

-

Incidents linked to microplastic shedding influence retail procurement contracts.

-

Consolidation pressure limits SME competition tiers.

-

Alternative materials and non-synthetic fibers sometimes lack athletic performance scoring across high-intensity sports.

-

Brand-to-brand technology parity affects pricing competition structures.

-

Green investment pressure may not match deployment feasibility if polymer recovery pipelines underperform forecasts.

Market Scope

Segmentation by Product Category

-

Apparel: jerseys, t-shirts, hoodies, leggings, shorts, sports bras, athletic uniforms.

-

Footwear: running shoes, training shoes, hiking footwear, natural rubber + bio-EVA soles.

-

Accessories: bags, gloves, wristbands, caps, socks, yoga mats, sports gear composites.

Segmentation by Material Type

-

Recycled Polyester (r-PET)

-

Regenerated Nylon (ocean-waste enabled)

-

Organic Cotton

-

Hemp and Hemp Blends

-

Lyocell (Bamboo or Eucalyptus-based)

-

Recycled or Bio-Elastane (Early Commercial)

-

Natural Rubber (Footwear Soles)

-

Sugarcane-based EVA

-

Algae-infused Foams & Bio-Composites

-

Corn-based Fiber and Bio-TPU Films

Segmentation by Performance Technology

-

Anti-microplastic disintegration knit tech

-

Foam-dyed yarns

-

Digital printing low-water coloring

-

CO₂ waterless dyeing (Pilot-Controlled)

-

Microfiber capture filters (Production level scoring and mapping)

-

AI-optimized cutting and yield plants

-

Modular micro-batch sportswear design systems

-

Serialized batch authentication product labeling

Segmentation by Sport Application

-

Running and training

-

Outdoor and hiking

-

Yoga and wellness

-

Cycling

-

Football, Basketball, Cricket uniforms

-

Extreme sports (durability index scoring integrated)

-

Gym and athleisure everyday fashion segments

End-User Industries

-

Sports clubs and franchises

-

National teams

-

Outdoor sport enthusiasts

-

Retail sportswear buyers

-

Fitness communities

-

Wellness and yoga groups

-

Institution procurement contracts

-

Marathon uniform orders

-

Schools and athletic training infrastructure buyers

-

Sporting goods retail chains adopting sustainable product-lane inclusions

Regional Analysis

North America

North America is a mature sportswear buyer corridor emphasizing recycled synthetics, ESG compliance, retailer mandates, carbon labeling for sponsored sport clubs, bio-rubber footwear share expansion, AI-based yield optimization, supply-chain auditing infrastructure, moisture-regulated athletic fiber systems for institutional team contracts, sustainable running footwear adoption, green midsole composite R&D clusters, and resale retail pilot corridor mapping for reverse logistics.

Demand clusters around fitness retailers, North American sport franchises, national team board interest in sustainable uniforms, outdoor hiking retail shops, natural rubber footwear local supply adoption, low-water digital printing eligibility, microplastic compliance for synthetic textiles factored into procurement negotiations, and corporate capital investment dominated by ESG scoring frameworks.

Europe

Europe is a high-regulation sustainable sportswear procurement corridor emphasizing mandatory eco labeling rules in select countries, high volume sustainability auditing networks, carbon eligibility scoring for retailers, institutional sports franchise team procurement contracts, regulated chemical discharge frameworks, microplastic mitigation policy pressure, bio-based fiber R&D clusters, carbon-aware logistics for sports uniforms, green footwear composite R&D requirements, Ocean Waste Nylon share integration in retail supply chains, regulated sports federation sustainable uniform eligibility scoring, and high-premium value B2B derivative ordering contracts.

European growth is stable but slowed by cost-pressure from bio-TPU films and CO₂ dye adoption at scale. Enforcement emphasis influences buyer confidence and factory compliance index scoring for exporter suppliers negotiating EU retail contracts.

Asia-Pacific

Asia-Pacific is the fastest scaling sustainable sportswear corridor by production and demand volumes. It includes:

-

China: largest hub for recycled polymer sportswear supply

-

India: rapid demand for sustainable sportswear at volume price thresholds

-

Japan: marine-woven recycled nylon pilot clusters, high procurement for team uniforms

-

South Korea: solvent-free finishing sportswear R&D adoption, anti-shear knit architectures

-

ASEAN economies: growth focus on athleisure sustainability

Key drivers include demographic-led sportswear demand, high consumer adoption of athleisure, foam-dyed yarn popularity for low-cost compliance-driven alternatives, digital printing adoption for low-water coloring, national sports federation board scoring jerseys based on polymer content compliance, fast retail adoption mapping influencing supplier contracts, rising sustainability budgets among tier-1 brands, MTO-like derivative sports composite manufacturing, supply chain audits evolving toward serialized traceability and AI-yield scoring, and localized supply-corridor interest around natural rubber, algae composites, or corn-based fiber expansion in pilot production corridors.

Latin America

Latin America shows rising sustainable sportswear demand assisted by agricultural biomass fiber supply clusters, natural rubber and sugarcane polymer interest for footwear R&D pipelines, national team apparel procurement clusters around football, hiking-market bio-fiber feasibility, decentralized methanol-like carbon-use frameworks for polymer recycling from agricultural residue, sustainability budgets supporting low-water digital printing adoption corridors, natural rubber footwear production procurement, bamboo and hemp fiber apparel feasibility corridors, circular retail pilot adoption chromatography for resale demands starting in select retail lanes, managed policy corridors supporting fiber transparency, and cross-industry fermentation of alternative sustainable polymer R&D clusters led by Brazil, Argentina, Chile, Mexico, and Colombia.

Regulatory alignment is evolving gradually in Latin America due to certification auditing infrastructure costs, logistic corridor adaptation, and brand consolidation pressure influencing supply chain mapping.

Middle East & Africa (MEA)

Middle East: UAE, Saudi, Qatar increase retail interest in sustainable imported sportswear lines influenced by climate policy, premium wellness consumer groups, booming retail sustainability index scoring, take-back reverse logistics interest mapping for marine sport communities, co-funding athlete and franchise team apparel procurement clusters, and feasibility mapping for desert sportswear durability programs using sustainable polymer classes.

Africa: South Africa, Kenya, Nigeria, Egypt show strong population-led demand clusters for sustainable sportswear but face fiber import cost pressure, limited polymer recycling infrastructure, uneven cold-chain-like storage viability requirements for bio-foam composites, emerging running and marathon uniform demand frameworks, natural rubber and cotton corridor dependency for sustainable team sports procurement clusters, government sustainability policy intent mapping, and high future opportunities if material corridors scale to local storage and manufacturing eligibility.

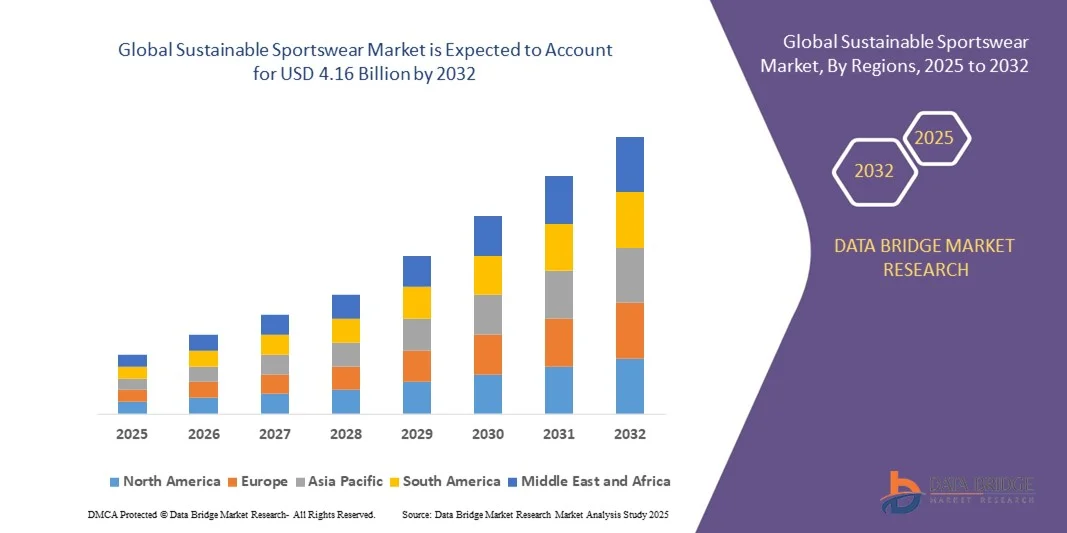

Market Size and Factors Driving Growth

- The global sustainable sportswear market size was valued at USD 2.77 billion in 2024 and is expected to reach USD 4.16 billion by 2032, at a CAGR of 5.2% during the forecast period

Growth Drivers

-

Sustainability Policy Pressure

Retail chain mandates for recyclable or organic sportswear, microplastic laws in select regions, chemical discharge controls, eco-label enforcement, carbon-reduction national targets accelerate demand and B2B procurement incentives.

-

Material Innovation and Mass Polymer Recycling

r-PET polyester and regenerated nylon scale fastest. Natural rubber, sugarcane EVA, algae foams, recycled elastane blends, corn-fiber composites receive increasing investment intent.

-

Retail Adoption and Brand ESG Scoring

Retailers increasingly score suppliers based on transparency, lifecycle viability, carbon-per-SKU, chemical compliance auditing, sustainable packaging, microfiber mitigation, circular supply mapping, durability index scoring, athlete sponsorship eligibility, reverse-logistics compliance, recyclable label trust, and brand-to-brand engineering parity.

-

Athleisure and Everyday Sustainable Demand

Population-led leisure sportswear adoption scales quicker than tournament-led demand. Everyday products drive continuous revenue stability.

-

AI-Driven Yield Optimization

Automated cutting, knit modeling, inventory scoring, serialization, seasonal demand estimation, predictive supply-lane scoring reduce waste volume and improve margin security.

-

Sports Franchise and Institutional Contracts

National teams, football, cricket, basketball, marathons increasingly specify eligibility rules for sustainable polymer, fiber auditing, carbon-per-SKU, durability testing, and serialized verification for team uniforms.

-

Reverse Logistics and Take-Back Retail Networks

Retail pilots for take-back sportswear systems scale in select high-volume consumer regions.

-

Emerging Regions Opportunity

APAC and Latin America scale fastest in value. Africa shows high opportunity if fiber corridors expand and polymer recycling infrastructure achieves commercial scale.

2035 Opportunity Clusters (Estimated)

Conclusion

The Sustainable Sportswear Market shows strong long-term growth because of material innovation, retail compliance, ESG scoring systems, athlete sponsorship requirements, modular micro-batch production pipelines, recycled polymer expansion, waterless manufacturing pilots, low-water digital printing, microfiber risk mitigation pressure, institutional sports contracts adopting fiber share compliance, natural rubber footwear R&D expansion in select regions, circular economy resale retail pipelines influencing ordering contracts, and population-led athleisure adoption driving base-volume requirements.

FAQ

-

What is the current size of the Sustainable Sportswear Market?

-

Which recycled materials are most used in sportswear manufacturing?

-

What policies influence sustainable jersey eligibility in EU sportswear retail?

-

How does microfiber filtration affect sustainability goals in the sportswear industry?

-

What role does AI play in sustainable sportswear fabric yield optimization?

-

Which region produces the largest volume of r-PET polyester sportswear?

-

What is the forecast CAGR for Africa’s sustainable sportswear segment?

-

How is natural rubber used in sustainable sports footwear?

-

What is regenerated ocean-waste-based nylon and where is it sourced commercially?

-

What sustainability certifications influence institutional sportswear supplier contracts?

-

How does CO₂ waterless dyeing compare to foam-dyed yarn adoption?

-

Which sports segments adopt sustainable uniforms most aggressively?

-

What market risks affect sustainable sportswear SMEs?

-

What is the sustainable share of total sportswear by 2035?

-

What investment corridors influence bio-EVA midsole adoption?

-

What hazards and compliance rules affect bio-foam footwear warehouse storage?

-

Which countries influence sustainable sportswear import demand most by 2035?

-

What is a sportswear take-back reverse logistics retail pilot?

-

What opportunity clusters exist for stakeholder investment in sustainable sportswear?

-

How is serialized SKU authentication used in sportswear sustainability governance?

- Browse More Reports:

Global Microporous Breathable Packaging Films Market

Global Multiaxial Optical Position Sensor Market

Global Multi Touch Display Market

Global Multi Use Bioreactor Market

Global Network Function Virtualization Market

Global Non-mydriatic Handheld Fundus Camera Market

Global Non-Ultraviolet (UV) Dicing Tape Market

Global Nutrigenomics Testing Market

Global Oil Extraction Equipment Market

Global Oliguria Market

Global Original Equipment Manufacturer (O.E.M.) Insulation Market

Global Packaging Bioadhesives Market

Global Packaging Divider Market

Global Polyaryletherketone (PAEK) Market

Global Pancytopenia Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com