Colorado Car Insurance Requirements 2026: Minimum Coverage Explained

Driving in Colorado isn’t exactly simple these days. Weather flips fast, traffic keeps growing, and costs… yeah, everything feels more expensive in 2026. If you’re trying to figure out Colorado car insurance requirements, you’re not alone. Most people only start looking into it after they get pulled over, buy a new car, or their old policy jumps in price for no clear reason.

Truth is, Colorado doesn’t try to overcomplicate things, but the rules still catch people off guard. And a lot of drivers think they’re covered when they really aren’t. That gap can hurt.

Colorado Minimum Coverage Basics (What the Law Actually Says)

Alright, here’s the core of it. Colorado requires liability insurance. That’s the baseline. Nothing fancy.

As of 2026, the standard minimums are:

-

$25,000 for bodily injury per person

-

$50,000 total bodily injury per accident

-

$15,000 for property damage

People call it “25/50/15.” Easy shorthand. But don’t let the simplicity fool you. These numbers don’t go very far anymore.

One bad accident, even a “small” one, and you’re already past $15k in damage. Modern cars are expensive to fix. Bumpers alone can cost more than you’d expect. And if someone gets hurt… yeah, those medical bills stack up fast.

Also, insurers in Colorado are required to offer uninsured/underinsured motorist coverage. You can reject it, but honestly, a lot of folks keep it because there are more uninsured drivers out there than people want to admit.

And yeah, this is where Colorado car insurance requirements get real. The law is just the starting point. Not the safe zone.

What Minimum Coverage Doesn’t Protect You From

This is where people mess up.

Minimum liability only protects other people. Not you. Not your car. Not your repairs.

So if you slide on black ice in winter (happens all the time), hit a pole, or your car gets stolen from a parking lot in Denver… you’re paying out of pocket unless you’ve added collision or comprehensive coverage.

And I’ll be blunt, a lot of drivers skip that extra protection to save money each month. It feels smart… until it isn’t.

Also, medical payments for you? Not included in basic liability. You’re kind of on your own unless you upgrade.

It’s one of those things nobody explains well at the dealership. Or they do, but too fast, and you just nod along.

Why Colorado Rules Feel Tight but Still Leave Gaps

Colorado tries to strike a balance. Not too strict, not too loose. But in practice, it leaves a lot of gray area.

You can legally drive with minimum coverage, sure. But “legal” and “protected” are two very different things.

And premiums are weird right now, too. Some ZIP codes in Colorado are way higher than others. Same driver, same car, totally different price depending on where you park at night.

Snow-heavy regions, urban traffic zones, and theft-prone areas all push rates around. It’s not always predictable either.

So yeah, people shop around a lot more in 2026. They have to.

Commercial Auto Insurance Colorado (For Businesses and Gig Drivers)

Now, if you’re using a vehicle for work, things change a bit. And this is where commercial auto insurance Colorado comes in.

If you’re running deliveries, contractors, rideshare work, or even just using your personal truck for business jobs, personal insurance might not cut it. Actually, most of the time it won’t.

Commercial policies are built for heavier use. More miles, more risk, more liability exposure. They usually come with higher limits and broader protection.

Think of it like this: your personal policy is for commuting and errands. Commercial coverage is for when your vehicle becomes part of your income stream.

A lot of small business owners in Colorado don’t realize this until they file a claim and get denied. Not fun. I’ve seen that happen more than once.

So if your vehicle is tied to work in any real way, it’s worth checking into commercial auto insurance Colorado options early, not after something goes wrong.

Common Mistakes Drivers Still Make in 2026

You’d think with all the info online, people would have this figured out by now. But nope.

A few things keep popping up:

First, people only buy the minimum and forget about everything else. Then they’re shocked when repairs aren’t covered.

Second, they assume “full coverage” means full protection. It doesn’t. That phrase is kinda misleading, honestly.

Third, they don’t update policies after life changes. New job, new car, new commute… same old insurance. That mismatch causes problems later.

And finally, people don’t compare enough. They stick with the same insurer for years, even when rates quietly climb.

Insurance isn’t something you set and forget. It shifts with your life.

Conclusion

At the end of the day, Colorado car insurance requirements are simple on paper but a bit trickier in real life. The state sets the minimum, but the real decision is how much protection you actually want when things go wrong.

Driving with just the basics keeps you legal, sure, but not always secure. And if you’re using your vehicle for business, don’t ignore commercial auto insurance Colorado options - it can be the difference between a small setback and a financial mess.

Not trying to scare anyone here. Just keeping it real. Insurance is one of those things you don’t think about… until you really, really have to.

Categorías

- Arts & Entertainment

- Causes

- Crafts

- Dance

- Drinks

- Film

- Health

- Food Trends

- Gaming

- Home & Garden

- Health & Fitness

- Literature

- Music & Concerts

- Networking

- Other

- Party

- Religion

- Shopping

- Sports

- Theater

- Wellness

- Cryptocurrency

- NFT Trends

- Coin update

- Lifestyle

- Business & Finance

- Entrepreneurship

- Marketing Strategies

- Personal Finance

- Investment Tips

- Industry Trends

- Technology

- Gadgets & Reviews

- Software & Apps

- Cybersecurity

- Emerging Technologies

- How-To Guides

- Educación

- Movie & TV Reviews

- Celebrity News

- Book Reviews

- Personal Development

- Motivation & Inspiration

- Life Hacks

- Community & Culture

- Local Events

- Cultural Insights

- Social Issues

- Interviews & Spotlights

- Volunteering & Activism

- Science & Nature

- Animal Behavior

- Beauty Tips

- Fashion Trends

- Product Reviews

- Food & Drink

- Cooking

- Restaurant Reviews

- Travel

- Arts & Crafts

- Photography

- Workout Routines

- Parenting Tips

- News

- Tips & Tricks

- Case Studies

- Product Reviews

- Interviews

- Opinion

- Research & Insights

- Events Coverage

- Personal Stories

- Anuncios

- Trends & Predictions

- Guest Posts

Read More

Nexagen: Suplemento de Mejora Masculina Nexagen Testosterone Booster es un suplemento alimenticio diseñado para mejorar la salud y el rendimiento masculino. A menudo se comercializa como una solución para aumentar la libido, mejorar la energía, y promover una mejor circulación sanguínea, todo con el objetivo de mejorar la función sexual y la vitalidad...

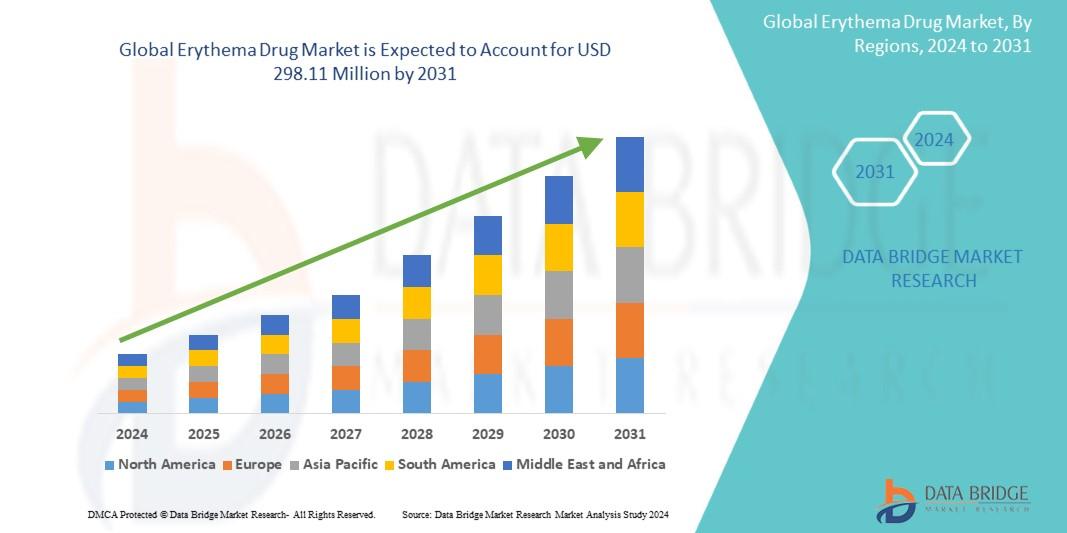

The Erythema Drug Market sector is undergoing rapid transformation, with significant growth and innovations expected by 2031. In-depth market research offers a thorough analysis of market size, share, and emerging trends, providing essential insights into its expansion potential. The report explores market segmentation and definitions, emphasizing key components and growth drivers....

Searching for a reliable Chiropractor Indianapolis Indiana? Integrated Health Solutions provides personalized care for back pain, neck pain, pregnancy discomfort, and injury recovery. Our patient-centered approach focuses on restoring spinal alignment, improving mobility, and supporting long-term wellness for individuals and families throughout the Indianapolis community.

Dairy Testing Market Overview: Jadhavar Business Intelligence is a Business Consultancy Firm that has published a detailed analysis of the “Dairy Testing Market”. The report includes key business insights, demand analysis, pricing analysis, and competitive landscape. The analysis in the report provides an in-depth aspect at the current status of the Dairy Testing Market....

Executive Summary Wi-Fi Range Extender Market Data Bridge Market Research analyses that the Wi-Fi range extender market was valued at USD 3600 million in 2021 and is expected to reach the value of USD 5913.38 million by 2029, at a CAGR of 6.4% during the forecast period. Today’s businesses choose the market research report solution such as Wi-Fi Range Extender Market report because...