Kategorien

- Arts & Entertainment

- Causes

- Crafts

- Dance

- Drinks

- Film

- Health

- Food Trends

- Gaming

- Home & Garden

- Health & Fitness

- Literature

- Music & Concerts

- Networking

- Andere

- Party

- Religion

- Shopping

- Sports

- Theater

- Wellness

- Cryptocurrency

- NFT Trends

- Coin update

- Lifestyle

- Business & Finance

- Entrepreneurship

- Marketing Strategies

- Personal Finance

- Investment Tips

- Industry Trends

- Technology

- Gadgets & Reviews

- Software & Apps

- Cybersecurity

- Emerging Technologies

- How-To Guides

- Ausbildung

- Movie & TV Reviews

- Celebrity News

- Book Reviews

- Personal Development

- Motivation & Inspiration

- Life Hacks

- Community & Culture

- Local Events

- Cultural Insights

- Social Issues

- Interviews & Spotlights

- Volunteering & Activism

- Science & Nature

- Animal Behavior

- Beauty Tips

- Fashion Trends

- Product Reviews

- Food & Drink

- Cooking

- Restaurant Reviews

- Travel

- Arts & Crafts

- Photography

- Workout Routines

- Parenting Tips

- News

- Tips & Tricks

- Case Studies

- Product Reviews

- Interviews

- Opinion

- Research & Insights

- Events Coverage

- Personal Stories

- Ankündigungen

- Trends & Predictions

- Guest Posts

Mehr lesen

Wood tiles, a versatile and increasingly popular design choice, offer homeowners the warmth and natural beauty of wood with the durability and practicality of tile. Whether used for flooring or wall coverings, they can transform a space, creating a striking visual impact and a lasting impression. This article explores how to leverage wood tiles to create a statement in your home. ...

Bomber jackets have become a wardrobe essential for women who want style, comfort, and versatility all in one piece. Whether running errands, heading to work, or meeting friends for coffee, a bomber jacket can instantly elevate a simple outfit. Its casual yet chic appeal allows women to mix and match with various pieces while staying comfortable throughout the day. This article explores...

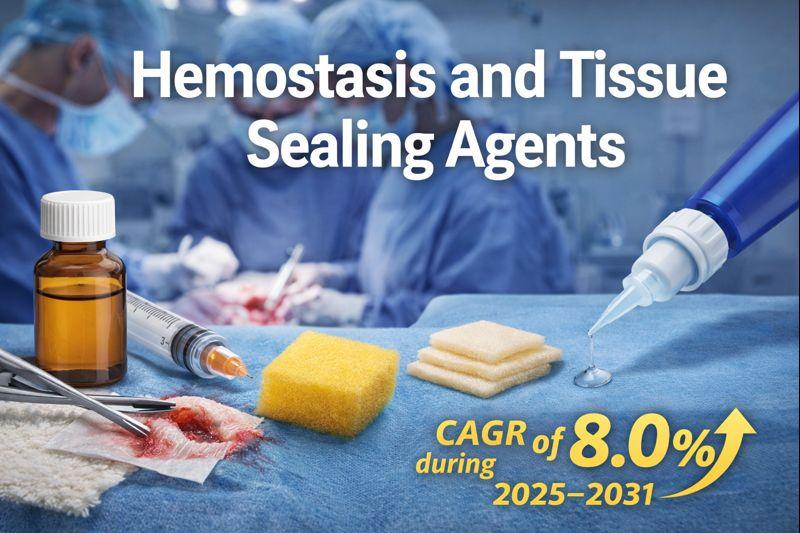

Hemostasis and Tissue Sealing Agents are specialized medical products used to control bleeding, seal tissues, and support wound closure during and after surgical procedures. They are essential tools in modern healthcare, helping surgeons improve outcomes, reduce complications, and speed up patient recovery. Market Growth Outlook The Hemostasis and Tissue Sealing Agents Market is...

Right-hand drive (RHD) cars have become increasingly popular among car enthusiasts, collectors, and drivers seeking something unique on the road. If you’re searching for right hand drive cars for sale, it’s important to understand the options available, pricing, and factors to consider before making a purchase. Why Choose Right Hand Drive Cars? Right-hand drive vehicles are standard...

Global common sucker rod market demonstrates steady growth fundamentals, valued at USD 1.23 billion in 2026 with projections indicating expansion to USD 1.56 billion by 2034, reflecting a CAGR of 4.05%. This sustained demand stems from the essential role sucker rods play in artificial lift systems within oil extraction operations worldwide. While mature oilfields require enhanced recovery...